INSIDER PERSPECTIVES

FOR CAPITAL INVESTMENT STAKEHOLDERS

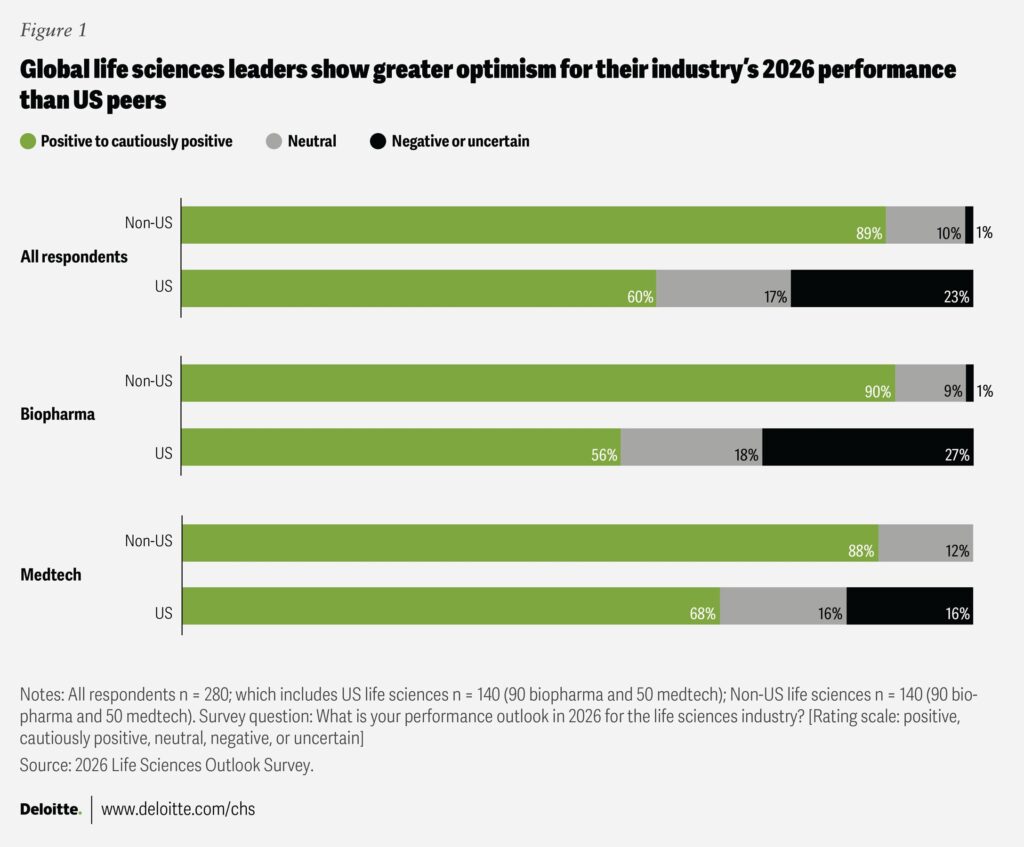

Regulatory scrutiny. Scientific breakthroughs. Market saturation in once-lucrative therapeutic areas. Few industries experience change at the velocity pharma and biotech do, and in 2026, that pace is accelerating rather than stabilizing.

Several years removed from the pandemic, leaders are reassessing where capital truly creates value. AI is reshaping drug discovery. Advanced modalities are redefining what “curative” means. Governments are rewriting pricing frameworks. And capital itself is more expensive than it was for most of the last decade.

In this edition of Capex Confidential, we take a look at how pharma and biotech leaders are rethinking capital allocation amid real opportunities and intensifying risks, and what finance, operations, and IT leaders must do differently to stay ahead.

Opportunities: Where Smart Capital Is Moving

Less Crowded Markets and the Return of “White Space” Investing

For much of the last two decades, capital flowed toward the largest and most predictable patient populations. Oncology, cardiometabolic disease, and autoimmune disorders attracted enormous investment and delivered blockbuster drugs. But success bred saturation.

PwC notes that therapeutic crowding increasingly leads to higher commercialization costs, lower peak sales, and margin compression, as multiple companies pursue similar patient populations and mechanisms of action (PwC, 2026). In response, many organizations are rediscovering the strategic appeal of white-space markets, underserved or previously overlooked patient populations with high unmet need.

Rare diseases illustrate this shift. While each indication may be small on its own, advances in genomics, diagnostics, and regulatory incentives have made these markets commercially viable at scale. Orphan drugs are now expected to represent more than 20% of global prescription drug sales by the end of the decade, supported by premium pricing and longer exclusivity periods (Evaluate Pharma, 2025).

GLP-1 receptor agonists offer a modern case study. Initially developed for type 2 diabetes, these therapies unlocked adjacent markets in obesity, cardiovascular risk reduction, and potentially neurodegenerative disease. Similarly, Alzheimer’s, once considered too risky to justify sustained investment, is re-emerging as a viable frontier as biomarker-driven trials and disease-modifying therapies advance (PubMed Central, 2025).

Capital implication: White-space investments carry higher scientific and execution risk, but they also offer longer-lived returns, less competitive pressure, and stronger pricing power. For capital planners, this raises the stakes around portfolio visibility, understanding not just project cost, but long-term strategic value.

AI-Powered Drug Discovery Becomes Core Infrastructure

The economics of drug discovery have historically been unforgiving. Industry estimates still peg the average cost of bringing a drug to market at over $2 billion, accounting for failures, with timelines of 12–15 years (DiMasi et al., 2016). Artificial intelligence is not eliminating those challenges, but it is reshaping them.

By 2026, AI will no longer be experimental. PwC emphasizes that future-leading pharma companies will be “AI-native,” embedding advanced analytics and machine learning across R&D, manufacturing, and commercial operations, not treating AI as a standalone tool (PwC, 2026).

The numbers reflect this shift. The AI-in-pharma market is projected to grow at nearly 20% annually through the mid-2030s, driven by faster target identification, improved clinical trial design, and more efficient manufacturing processes (PharmiWeb, 2025). Reuters reports that large pharma companies are now investing in AI as foundational infrastructure, aiming to compress early-stage development timelines and reduce late-stage failure rates (Reuters, 2026).

Examples continue to validate the promise. Insilico Medicine leveraged generative AI to identify a clinical candidate for idiopathic pulmonary fibrosis in under three years, a process that traditionally would have taken far longer and cost significantly more. Exscientia reports reducing early molecule design timelines from 4.5 years to as little as 12–15 months using AI-driven platforms (Exscientia, 2023).

Still, faster discovery introduces new capital challenges. Accelerated pipelines compress downstream timelines, often requiring earlier investment in clinical operations, data infrastructure, and manufacturing capacity. AI also introduces regulatory, ethical, and governance considerations that demand ongoing investment.

Capital implication: AI is not just an R&D efficiency play. It is an enterprise-wide investment that reshapes how and when capital should be deployed and rewards companies that plan holistically rather than project by project

Advanced Modalities: Scientific Breakthroughs Meet Balance Sheet Reality

The promise of next‑generation therapies, including gene editing, cell therapies, and advanced biologics, remains one of the most compelling growth avenues in pharma and biotech. Cell and gene therapy funding reached approximately $11.1 billion across 216 deals in 2025 (PharmaSource, 2026), reflecting sustained investor interest even amid broader market headwinds, and signaling continued commitment to these modalities as strategic growth engines. However, this enthusiasm comes with escalating technical and financial challenges as these treatments move out of the lab and into commercial production.

From a capital planning perspective, the industrialization of advanced modalities is both an opportunity and a challenge:

- Market expansion and clinical progress: Cell and gene therapy sectors have shown strong growth in financing and pipeline depth, with continued uptake of CRISPR, CAR‑T, and other precision platforms (PharmaSource, 2026).

- Manufacturing complexity: Rapid scientific progress has outpaced the establishment of standardized production systems. Customized viral vector manufacturing, specialized fill‑finish processes for biologics and ADCs, and quality systems that meet global regulatory expectations all demand significant Capex and operational expertise. Surveys of industry leaders show that manufacturing agility, the ability to ramp and scale production rapidly, remains a key bottleneck due to variability in processes and talent shortages (Pharma Manufacturing, 2025).

- Capital intensity and infrastructure needs: The materials, facilities, and capability investments required for advanced therapies remain structurally higher than those for traditional small‑molecule drugs. Biotech firms often partner with CDMOs, but even outsourced models can involve significant upfront commitments and long‑lead financing (Pharma Manufacturing, 2025).

Capital implication: Investing in advanced modalities now means balancing frontloaded Capex for infrastructure with long‑term value from differentiated therapeutics and planning carefully around operational readiness, talent development, and scalable manufacturing strategies.

Threats: Where Capital Risk Is Rising

Regulatory and Pricing Uncertainty Remains the Constant

Capital planning in 2026 is complicated by an unpredictable regulatory landscape. According to a recent survey of more than 1,200 biopharma executives, 51% believe government policy is currently inconsistent and fragmented, up from 45% in 2023, and half say the policy environment makes it harder to raise capital (Fierce Pharma, 2025). Fragmented policy can affect everything from clinical trial continuity to talent decisions and cross‑border development strategies.

In addition, pricing and reimbursement risk, particularly for high‑cost, innovative therapies, persists as a key concern for investors and management teams. Biologic drugs face pricing pressure from payers and health technology assessment bodies that increasingly demand evidence of cost‑effectiveness, while initiatives to expand biosimilars could further erode revenue for branded products when patents expire. One industry analysis estimated that biosimilars have already delivered billions in cost savings, but that market uptake remains limited by regulatory complexity and payer reluctance.

Capital implication: Regulatory and pricing uncertainty affects near‑term cash flow projections and long‑range forecast models. Capital allocators must incorporate broad policy scenarios into financing plans, including potential delays in approvals, shifts in reimbursement frameworks, and changing payer incentives to protect portfolio value and maintain strategic optionality.

The Rising Cost of Complexity

As the industry pursues increasingly complex therapies and global market access, the cost structure of innovation continues to rise. A 2025 industry survey of biopharma leaders found that manufacturing agility, a proxy for operational resilience and capital efficiency, has declined in recent years, driven in part by skill shortages and regulatory fragmentation. Approximately one‑third of firms reported slow ability to scale production for modalities like cell therapy and mRNA, highlighting the capital strain of maintaining flexible manufacturing capacity while complying with evolving standards (Pharma Manufacturing, 2025).

This complexity has real financial implications:

- Specialized manufacturing systems for cell and gene therapies often require bespoke equipment, clean‑room environments, and talent that command premium compensation.

- Supply chain challenges, especially for biologics and advanced modalities requiring cold‑chain logistics, add layers of cost and risk.

- Regulatory requirements across regions continue to diverge, imposing additional compliance costs and delaying global launches.

Capital implication: The industry’s cost base is being driven upward by regulatory, manufacturing, and supply chain complexity. Allocators must differentiate between investments that materially enhance capacity and those that simply maintain the status quo. Incremental Capex decisions made without an integrated view of enterprise risk may erode competitive advantage rather than build it.

The Enterprise View: Finance, Operations, and IT

Finance: From Budgeting to Capital Activism

With revenue growth less predictable, finance teams are shifting from static annual budgets to capital activism, actively reallocating funds toward initiatives that deliver the strongest strategic and financial returns.

According to Deloitte (2025), nearly half of life sciences executives are using digital tools and AI to improve productivity and ROI, but only a minority have fully scaled these investments. Rolling forecasts, scenario planning, and dynamic reprioritization are now essential for aligning capital with measurable value across R&D, operations, and commercial strategy.

Bottom line: Finance is no longer just reporting costs; it’s driving enterprise-wide value by allocating capital where it matters most.

Operations: Resilience Is Now a Capital Decision

Supply chain disruptions, geopolitical uncertainty, and pandemic-era lessons are reshaping how pharma and biotech approach operational strategy. Companies are no longer treating manufacturing location decisions as purely operational choices; they are strategic capital decisions. A surge of U.S. and regional investment illustrates this shift:

- Roche/Genentech is investing $2 billion in North Carolina to expand biomanufacturing capacity and reduce reliance on global supply chains. (Reuters, 2026)

- Moderna is committing $140 million to complete its domestic mRNA manufacturing network, consolidating end-to-end production to mitigate global disruptions. (Reuters, 2025)

- Eli Lilly announced a $6 billion API manufacturing facility in Alabama as part of a broader U.S. production expansion strategy. (Reuters, 2025)

- Industry analysts estimate that over $370 billion in U.S. biopharma manufacturing investments are planned to bolster resilience and diversify production away from high-risk regions. (FiercePharma, 2025)

These onshoring, nearshoring, and “friend-shoring” initiatives carry significant near-term Capex, but they also reduce long-term operational and geopolitical risk, enabling companies to better control quality, continuity, and speed to market. For capital planners, the takeaway is clear: resilient operations require deliberate, strategic capital allocation, not ad hoc spending.

IT: Infrastructure Is Strategy

As innovation increasingly relies on AI, real-world data analytics, and cloud-based R&D platforms, IT is no longer a supporting function; it has become a strategic driver of enterprise value.

- Cybersecurity risks are escalating. In 2025, ransomware and phishing attacks caused temporary shutdowns at multiple pharma manufacturing sites, delaying clinical trial supply chains and putting patient timelines at risk. (IBM X-Force, 2025)

- AI-driven R&D workloads now require high-performance, scalable, and secure cloud infrastructure. Pharmaceutical AI pipelines from molecular modeling to clinical trial simulation can generate petabytes of sensitive data, making infrastructure investments non-negotiable. (PwC, 2026)

- Underinvesting in IT now may save short-term dollars, but it amplifies risk: slower drug discovery, potential regulatory noncompliance, compromised patient data, and erosion of trust.

Capital implication: IT and digital infrastructure must be treated like core physical assets. Investments in secure, scalable, and integrated systems are strategic enablers of faster, safer, and more efficient R&D, manufacturing, and commercial operations.

The Bottom Line

Pharma and biotech are entering a new era, one defined less by scientific ambition alone and more by capital precision. Innovation remains essential, but it is disciplined, agile capital allocation that determines which breakthroughs become durable businesses.

With development cycles accelerating and regulatory scrutiny intensifying, leaders need real-time visibility into where capital is deployed, how projects interconnect, and which investments truly drive long-term value. Platforms like Finario enable that clarity, helping turn capital planning from a constraint into a competitive advantage.