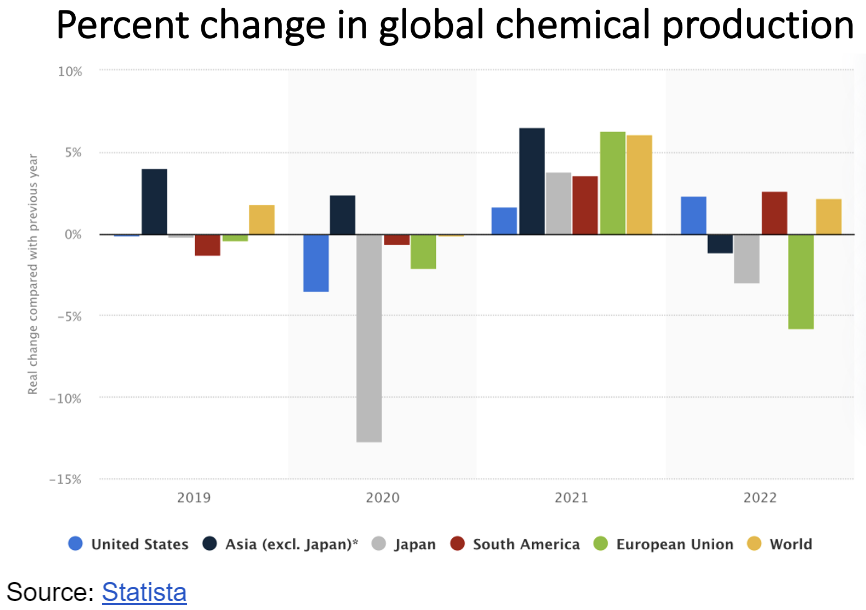

Strong demand and higher prices made 2022 a good year for the global chemicals industry overall, but results varied widely by region. In the U.S., the sector had “one of its best years in a decade,” while European companies struggled to navigate an energy crisis.

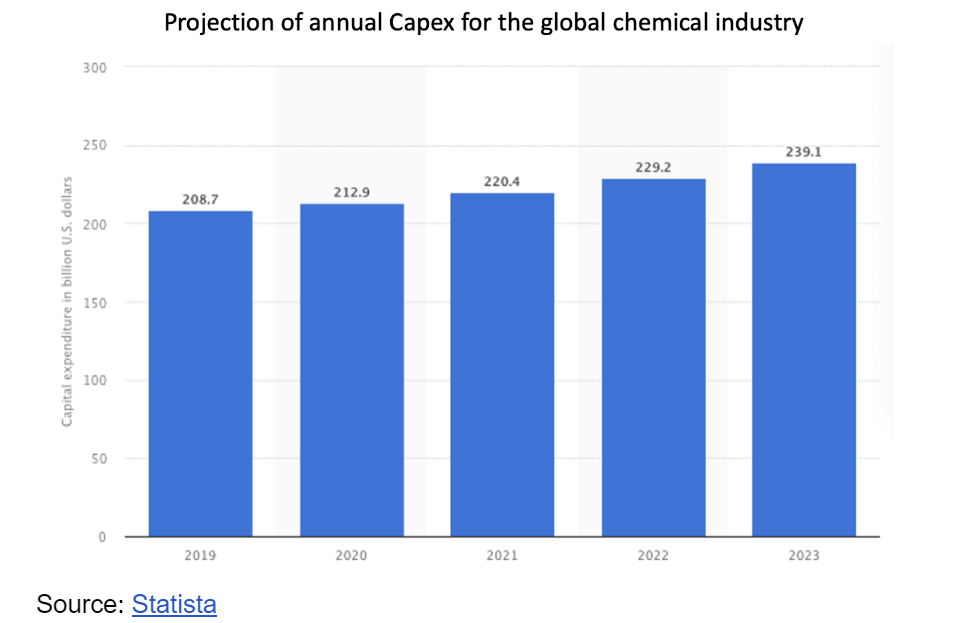

With a recession expected by many in 2023 or early 2024, the near-term future of the industry is uncertain. However, many producers remain committed to bold capital projects that will spur organic growth and make themselves more sustainable.

In this deep dive, we’ll explore the crossroads that the chemicals industry finds itself in, and the key trends capital planners should keep an eye on to maximize their Capex performance throughout the 2020s and beyond.

Climate change is an issue that nearly all industries are trying to get their arms around, but it’s a particular focus for the chemicals industry. According to the International Energy Agency (IEA), “the chemical sector is the largest industrial energy consumer and the third largest industry subsector in terms of direct CO2 emissions. This is largely because around half of the chemical subsector’s energy input is consumed as feedstock – fuel used as a raw material input rather than as a source of energy.”

A range of stakeholders—including governments, investors, and regulators—are sounding the alarm and demanding big changes. As consultancy Oliver Wyman points out, “failure to meet sustainability targets represents the single greatest long-term risk to [chemical] companies, putting even their license to operate in jeopardy. Companies that fail the sustainability test may find themselves locked out of financing, especially as banks and other institutional investors focus on greening portfolios and making ESG priorities core to investment strategies.”

Industry leaders have recognized the urgent need to decarbonize their operations, and are responding with bold capital investments. Dow Chemical, the biggest producer in the U.S., has a goal of spending around $1 billion per year on decarbonization projects, and is planning on constructing the “world’s first net-zero carbon emissions ethylene and derivatives complex” in Canada in 2023. Despite job cuts to start the year, the company has reaffirmed its expectation that Capex spending will increase by 21% in 2023.

It’s not just American firms that have ambitious capital spending goals. German chemical company BASF will invest over $25 billion through 2025 with the goal of driving organic growth, and has announced plans “to build a new hexamethylene diamine (HMD) plant in France and expand Polyamide 6.6 production at its facility in Freiburg, Germany.” Netherlands-based LyondellBasell spent around $2 billion in Capex in 2022, with a relatively even split between growth and maintenance projects. Going forward, the company expects capital spending to remain at that level for the next several years, and “accelerate its investments in decarbonization in the latter half of the 2020s.”

Powder & Bulk Solids, a magazine focused on the chemical and related industries, summed up the outlook going forward:

“Across the chemical industry, manufacturers are building new facilities to support growth, improving their existing asset bases, and investing in sustainability-related initiatives. As the decade progresses, Powder & Bulk Solids expects to see a greater share of Capex go toward assets that support the circular economy and furthering the decarbonization of chemical operations.”

While decarbonizing their operations will be a significant challenge for chemical companies, it also presents an enticing opportunity as demand for battery materials surges. BASF expects that “its Battery Materials business will become ‘a significant earnings contributor’” to its portfolio, and is planning to invest up to $5 billion in Capex between now and 2030.

A number of Korean companies are also seeing the opportunity in batteries. Lotte Chemical has committed nearly $8 billion to new battery material and hydrogen projects by 2030, and “plans to open American production facilities for battery materials in a few years.” Additionally, LG Chem has set aside $5.2 billion to expand its battery materials unit, and POSCO chemical is building a battery cathode materials plant in Canada through a joint venture with General Motors.

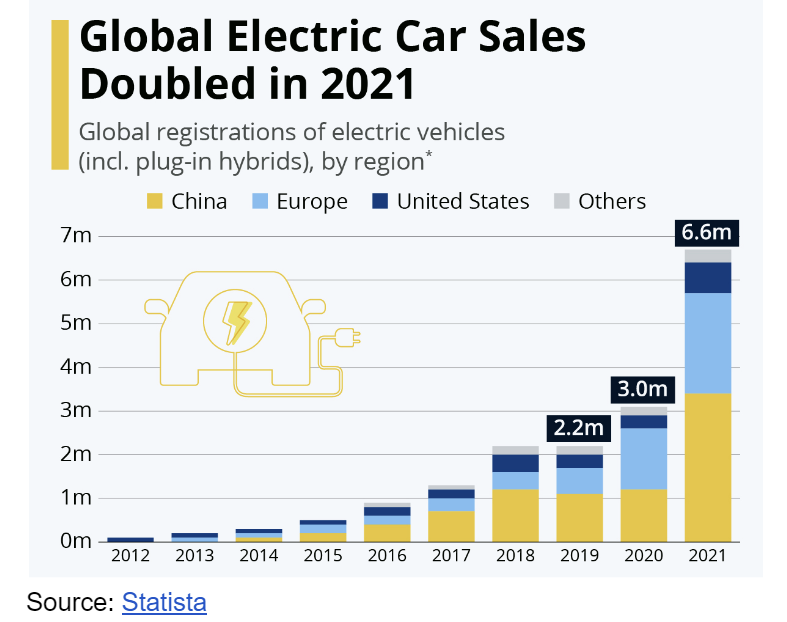

The main driver behind all of this battery demand is electric vehicles (EVs). While just one in seven passenger cars sold globally was an EV in 2022, demand has been growing exponentially, and producers are seeing the writing on the wall.

On top of the Inflation Reduction Act (IRA), which provided a number of incentives for both producers and consumers of EVs, the Biden administration recently proposed even more ambitious legislation “designed to ensure two-thirds of new passenger cars and a quarter of new heavy trucks sold in the United States are all-electric by 2032.” As a result, “battery manufacturing is ramping up across the [U.S.]” and in many regions around the globe.

The chemical industry’s transition towards battery-powered solutions marks a pivotal step in embracing a sustainable, low-carbon future. The scale of this transition is so massive that chemical company leaders ought to think about these Capex projects as their own category.