FP&A’s Moment: Why Capital Planning Is the Function’s Highest-Stakes Opportunity … and Biggest Vulnerability

You know what the board is going to ask.

Which projects are still the right ones? How are you prioritizing? What’s the ROI on AI? What happens if conditions change? How does FP&A inject itself into capital decisions in real time?

That last question is the one FP&A professionals should be losing sleep over. Because for most finance teams, the honest answer is: not as much as it should.

That’s not a criticism. It’s a structural reality. For decades, FP&A has been organized around a downstream model: business units make capital decisions, finance models the outcomes, and FP&A reports on variances after the fact. The process made sense when capital decisions were relatively stable, and the forecasting horizon was predictable.

Neither of those conditions exists anymore. And FP&A teams that don’t make the shift from downstream reporter to upstream strategic partner are going to find themselves increasingly irrelevant to the decisions that matter most — and increasingly exposed when those decisions go wrong.

Capital planning is the arena where that shift is most consequential. Here’s why — and what it takes to get it right.

The downstream trap: how FP&A gets cut out of capital decisions

The downstream model has a certain logic to it. Business units are closest to the operational reality. Engineering knows what equipment is needed. Operations knows what’s failing. IT knows where the technology gaps are. Finance’s job, in this model, is to evaluate the financial merit of proposals that arrive pre-formed and to aggregate the approved ones into a capital budget.

The problem is that by the time capital proposals reach FP&A for evaluation, the most important assumptions have already been made. The project scope is defined. The strategic rationale is set. The preferred vendor is often already identified. FP&A is being asked to validate decisions, not inform them.

This matters because the assumptions baked into capital proposals are increasingly unreliable. According to a recent CFO priorities analysis, one of the clearest signals of a high-performing finance function is whether changing projections actually trigger operational adjustments — in capital deployment, hiring, and inventory — or whether the forecast remains a reporting exercise. In most organizations, it’s the latter.

The result: FP&A produces updated forecasts that reflect new realities. The capital portfolio doesn’t change. And six months later, everyone is surprised by the variance.

Why capital planning specifically is FP&A’s highest-stakes opportunity

Of all the domains where FP&A could play a more strategic role — revenue forecasting, workforce planning, scenario modeling — capital allocation is the one with the highest leverage and the longest consequences.

A wrong revenue forecast costs you a quarter. A wrong capital allocation decision can cost you three years and eight figures. Equipment that sits underutilized because the workforce plan wasn’t funded alongside it. A facility expansion that becomes a stranded asset when a customer relationship shifts. An automation investment that can’t be evaluated or course-corrected because it was approved outside the normal capital discipline framework.

These aren’t hypothetical risks. According to IBM’s 2026 FP&A Trends research, 69% of CFOs say AI is integral to their finance transformation strategy — but most organizations still lack the integrated planning infrastructure to connect capital decisions to live financial data. That means approved projects are running on stale assumptions, and nobody has a systematic way to know which ones.

The FP&A team that builds a seat at the capital planning table — upstream, not downstream — is the one that can flag those stale assumptions before they become expensive mistakes. That’s not a reporting function. That’s a strategic function. And it’s the highest-value thing FP&A can do in 2026.

What ‘upstream’ actually looks like in practice

Moving FP&A upstream in capital planning isn’t about reorganizing the org chart. It’s about changing where finance sits in the capital decision timeline, and what it brings when it gets there.

In practice, upstream FP&A in capital planning means four specific things:

1. FP&A stress-tests assumptions before approval, not after.

Every major capital proposal should undergo an FP&A assumption review before reaching the approval stage. Not to approve or reject the project — that’s the CFO’s call — but to surface the inputs that are most likely to change and quantify what happens to the project economics if they do. A proposed automation investment with a 4-year payback period at today’s labor rates looks very different if wages continue trending at the rate over the past three years. FP&A should be the team that runs the model and presents it to the decision-maker.

2. FP&A maintains a live view of the portfolio, not a static budget.

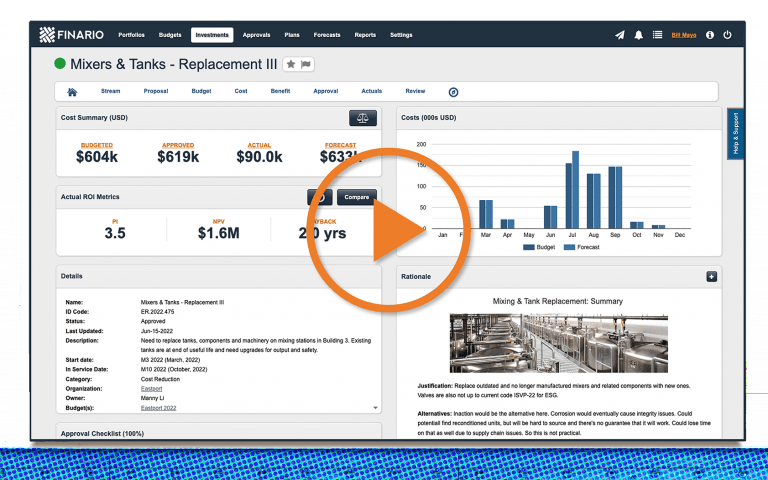

The capital budget approved in Q4 is a snapshot. The world it was built on keeps moving. FP&A’s job is to maintain a portfolio view that reflects current conditions — updated at a minimum quarterly — and to flag when material assumption changes would alter the ranking or viability of approved projects. This requires a single system of record for all capital projects, with documented assumptions and trigger conditions for each. It cannot be done in spreadsheets distributed across business units.

3. FP&A owns scenario modeling across the full capital portfolio.

When the board asks what happens to the capital portfolio if tariffs increase, or demand drops, or interest rates move — that answer has to come from FP&A. Not as a one-time exercise prepared for a board presentation, but as a standing capability. According to PPN Solutions’ 2026 FP&A Trends analysis, scenario planning is becoming a core FP&A responsibility, with finance teams expected to model multiple outcomes as routine, not just in response to a crisis.

4. FP&A participates in the Capex Council, not just the budget cycle.

The quarterly capital review — the Capex Council described in the main article — is where the upstream FP&A role gets institutionalized. When FP&A has a seat at that table, it can surface changed assumptions in real time, connect updated financial forecasts to specific project decisions, and provide the CFO with the analytical support needed to make — and defend — live portfolio adjustments. Without that seat, FP&A will always be reacting to decisions that have already been made.

The tool gap that makes all of this harder than it should be

Here’s the uncomfortable operational reality: most FP&A teams can’t play an upstream role in capital planning because they lack the tools to do so.

According to Deloitte’s Finance Trends 2026 research, 64% of finance leaders plan to add technical skills and capabilities to address persistent talent gaps — but talent alone doesn’t solve the structural problem. A skilled FP&A analyst working in disconnected spreadsheets, without a live view of the capital portfolio or a single system of record for project assumptions, cannot perform real-time scenario analysis across 30 capital projects. The math doesn’t work.

The Prophix 2026 FP&A Trends report puts it plainly: legacy tools don’t just slow insights — they create blind spots and bottlenecks. And in capital planning specifically, blind spots are expensive.

Purpose-built enterprise capital planning software changes the equation. It gives FP&A a consolidated, live view of the full portfolio. It documents assumptions and tracks actuals against forecasts in real time. It enables scenario modeling across the portfolio rather than on a project-by-project basis. And it connects capital decisions to the operational and financial data FP&A already owns — making the upstream role operationally feasible, not just theoretically desirable.

The career case for FP&A professionals

There’s a professional development dimension to this conversation that’s worth naming directly.

The FP&A function is at an inflection point. According to IBM’s FP&A Trends research, the most forward-looking finance organizations are repositioning FP&A as an orchestrator of insight rather than a producer of reports — connecting prediction with planning, and planning with decisions. That shift creates real career leverage for FP&A professionals who build capital planning capabilities.

The skills that matter most in upstream capital planning — assumption stress-testing, portfolio scenario modeling, cross-functional stakeholder management, and the ability to connect financial data to operational decisions — are exactly the skills that distinguish senior FP&A leaders from mid-level analysts. They’re also the skills that make FP&A professionals credible partners to the CFO, not just producers of the monthly deck.

FP&A professionals who own the capital planning process — who can walk a CFO through the portfolio logic, run a live scenario when the board asks, and flag a stale assumption before it becomes a variance — are the ones who will be in the room when the most consequential decisions are made.

The bottom line

Capital planning is not a back-office finance function. It’s the arena where FP&A can have the most strategic impact — and where the cost of sitting downstream is highest.

The five board questions in the main article aren’t just a checklist for CFO preparation. They’re a roadmap for what FP&A needs to deliver: a live portfolio view, consistent scoring criteria, documented scenario responses, and a real-time connection between financial forecasts and capital decisions.

Building that capability requires the right process, cadence, and technology. But it starts with a choice about where FP&A sits in the capital decision timeline.

Upstream or downstream. Strategic partner or variance explainer. The function gets to decide — but the window for making that choice is narrowing.

Watch our product

overview video