Top Down vs. Bottom Up: The Capex Budgeting Debate That Never Gets Old And Why It Matters More Than Ever Right Now

Let’s be honest with each other for a moment.

Every year, somewhere in an organization like yours, the same conversation happens. Finance sends down a number. Operations pushes back. Project teams either scramble to justify what they need or quietly pad their asks. And by the time the budget is “locked,” nobody’s entirely happy, and nobody’s entirely sure it reflects the company’s best thinking about where capital should actually go.

Sound familiar?

The good news is that this tension between the command-and-control certainty of a top-down budget and the grassroots realism of a bottom-up build isn’t a failure of process. It’s a signal. It’s your organization telling you that capital planning, as it’s currently structured, is leaving value on the table.

The question worth asking in 2026 isn’t which of these approaches is right. The question is: why are you still choosing only one?

The Landscape Has Shifted Under Your Feet

Before we get into the debate, let’s acknowledge the environment you’re operating in.

The global capital expenditure market was valued at approximately $1.48 trillion in 2024, and large enterprises alone accounted for between $740 billion and $1.15 trillion of that spending. That’s not small money. And the market is projected to grow at a CAGR of 3.93% through 2035, driven by the convergence of infrastructure modernization, digital transformation, and the sustainability imperative (Market Research Future, 2026).

At the same time, the cost of getting capital allocation wrong has never been higher. Tariffs can reshape Capex planning almost overnight. Since early 2025, the US weighted-average tariff rate has reached its highest level in a century, and the cascading effects through global supply chains are difficult to predict and even harder to budget around. As McKinsey has noted, companies that were considering putting capital into regions with unclear tariff scenarios have had to immediately rethink those decisions (McKinsey, 2025).

McKinsey’s research is direct on this point: achieving world-class Capex management can drive a 15 to 25 percent reduction in overall capital spend while simultaneously improving ROIC (McKinsey, 2019). That’s a significant number. And it begs the question: is your budgeting methodology the thing standing between you and that efficiency?

Here’s where the top-down versus bottom-up debate gets genuinely interesting.

The Top-Down Approach: Speed, Control, and the Danger of Inertia

The top-down model is intriguing. Leadership sets a number informed by strategy, financial targets, board expectations, and macroeconomic outlook, and the organization works within it. No sprawling wish lists. No endless justification cycles. Just a clear envelope and the expectation that business units get creative within it.

For companies navigating tight capital markets or executing a deliberate phase of financial consolidation, this makes sense. Chevron, for example, announced a 2025 Capex range of $14.5 to $15.5 billion, a $2 billion year-over-year reduction, with CEO Mike Wirth describing it as a demonstration of “commitment to cost and capital discipline” (Chevron, 2024). That kind of clarity from the top sends a message, internally and externally, about organizational priorities.

But here’s the thing about top-down budgeting that nobody in the budget meeting wants to say out loud: last year’s number is not a strategy. It’s institutional memory masquerading as a plan.

When a top-down allocation simply rolls forward prior-year spend adjusted for inflation, trimmed for optics, or inflated to account for known projects, it encodes the past into the future. The assets that needed investment three years ago are getting funded again. The breakthrough opportunity that emerged six months ago gets underfunded because it wasn’t in last year’s envelope. And the projects that should be killed because they no longer align with strategy? They can survive by default.

There’s also the risk that departments and business units default to doing things the way they always have, missing opportunities to become more efficient or more competitive. As one analysis puts it plainly: the biggest danger of incremental budgeting is that it funds history, not strategy. If a department was inefficient last year, it’s guaranteed to be inefficient this year, just with more money (Financial Models Lab, 2026). That’s not a planning process. That’s organizational gravity.

The Bottom-Up Approach: Accountability, Realism, and the Risk of Noise

If the top-down model suffers from inertia, the bottom-up model suffers from noise.

The theory is compelling: every capital project should be able to stand on its own merits. Business units submit requests grounded in operational reality, financial modeling, and strategic rationale. Finance consolidates, compares, and funds the best ideas. Capital flows toward the highest-value opportunities, not toward whoever controlled the budget last year.

In a true bottom-up process, each department identifies key spending categories: equipment, infrastructure, technology, and external vendors, and submits detailed cost estimates based on the headcount, tools, and programs they need to execute their plan for the year. McKinsey’s research finds that organizations frequently struggle with disparate project definition methods that prevent any single company-wide view of the capital portfolio, the very problem a disciplined bottom-up process, built on standardized taxonomy and project-level business cases, is designed to solve (McKinsey, 2017). The granularity can be a genuine asset. It surfaces priorities that executive leadership might otherwise miss. It gives project owners skin in the game. It creates a culture of accountability because teams have to justify what they’re asking for.

But the bottom-up model has a well-documented failure mode: when departments set their own budgets, they tend to build in buffers for unknown costs, leading them to request more than they need. Budgetary slack, once baked in, has a way of becoming permanent and growing over time. That can cause misallocation of budget and, on a broader scale, inefficiency (Financial Models Lab, 2026).

There’s also the consolidation problem. When fifty project requests land on finance’s desk with fifty different templates, fifty different ROI calculations, and fifty different definitions of “strategic priority,” you don’t have a capital plan. You have a negotiation. And negotiations reward the loudest voices and the best internal lobbyists, not necessarily the best projects.

McKinsey’s analysis of capital project delivery finds that cost and schedule overruns versus original estimates frequently exceed 50 percent, driven in no small part by unclear ownership, fragmented approval processes, and organizations committing to projects without adequate business case rigor (McKinsey, 2022). The bottom-up model, without a strong process architecture, can be its own worst enemy.

The Real Problem: You're Treating a Dynamic Situation as a Static One

Here’s the insight that ties this all together.

Both approaches, top-down and bottom-up, were designed for a world that no longer exists. A world where budgets were set once a year, reviewed at mid-year, and essentially frozen in between. A world where the strategic landscape shifted slowly enough that the plan you built in October was still basically valid the following September.

The traditional capital budgeting model, an annual ritual of spreadsheet-driven forecasts, approvals, and static allocations, is incompatible with today’s pace of change. Faced with geopolitical uncertainty, material price shifts, and unforeseen demand fluctuations, fixed annual Capex budgets simply can’t keep up (Finario, 2025). The organizations winning right now are those that have stopped asking “top-down or bottom-up?” and started asking: “How do we build a process that gives us both the strategic coherence of top-down thinking and the operational intelligence of bottom-up visibility and keeps both updated in real time?”

As the dust settles on many organizations’ budgeting seasons, public policies come into clearer view (or not), and macroeconomics continue to be unpredictable. Lingering questions remain for Capex stakeholders. If there has ever been a time to challenge your assumptions and address processes that once seemed workable but suddenly are not, it’s now (Finario, 2025).

That’s not rhetorical. Consider what’s currently driving capital investment decisions:

The Industry 4.0 tech market, including robotics, digital twins, and predictive systems, is forecast to grow from $551 billion in 2024 to $1.6 trillion by 2030, at a CAGR of 19.4% (Finario, 2025). The organizations that capture that opportunity are the ones making smart, well-timed capital commitments now, not the ones still waiting for the annual planning cycle to catch up to reality.

Meanwhile, businesses appear to have pent-up demand for Capex now that uncertainty has eased, with construction spending on healthcare, power, communications, and other structures poised to increase (LPL Research, 2025). The window for differentiated investment is open, but it won’t stay open forever.

The Third Way: Integrated Capex Planning Built for How the World Actually Works

So what does the better approach look like in practice?

It starts with a realization that’s simultaneously obvious and underappreciated: the goal of capital budgeting isn’t to produce a budget. It’s to produce the best possible allocation of finite capital against an evolving set of opportunities and constraints.

That reframing changes everything about how you design the process.

Strategic envelopes, not strategic straightjackets. The top-down element shouldn’t be a single number handed down from on high. It should be a set of strategically defined investment envelopes with investment thresholds, and customized by category, business unit, or priority tier that provide guidance without creating artificial constraints on the best projects. Leadership sets direction and boundaries. Business units operate with genuine latitude within them.

Standardized project justification, not ad hoc lobbying. Every project that enters the portfolio should be evaluated against a consistent framework: ROI methodology, risk scoring, strategic alignment criteria, and payback period. Standardized business case templates tailored to your organization’s taxonomy, data fields such as ROI models, and risk-scoring criteria ensure consistency, accuracy, and strategic alignment across all proposals (Finario, 2025). When you have a common language for capital, you can compare projects across the enterprise on their actual merits, not on the quality of the presentation deck.

Rolling forecasts, not annual snapshots. McKinsey’s research shows that companies that dynamically reallocate their capital, rather than locking in annual allocations and holding firm, outperform those that stay static, posting a median compound annual growth rate for total shareholder returns of 10 percent versus 6 percent for companies that did not reallocate (McKinsey, 2020). Rolling forecasts are how you operationalize that dynamism. Organizations that are winning the capital allocation game right now aren’t waiting for next year’s budget cycle to respond to this year’s opportunities; they’re operating with living forecasts that update as reality changes.

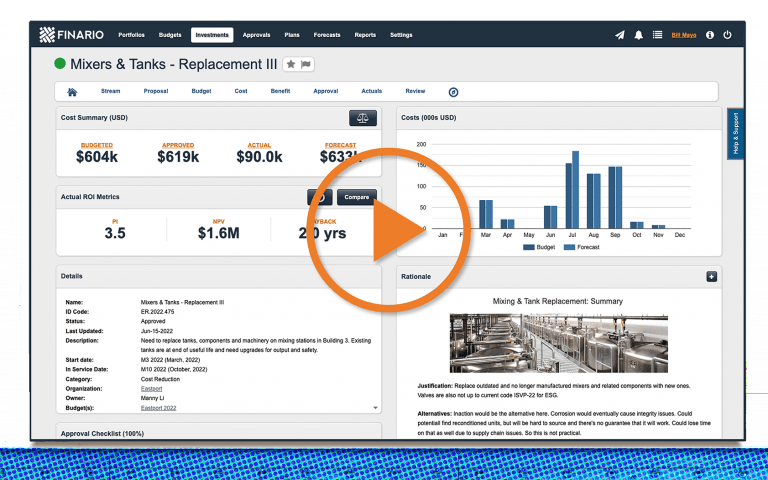

Real-time visibility across the portfolio. This is where the technology conversation becomes unavoidable. Managing all your capital investments within a single system, one that dynamically updates approval status, actual costs incurred, and other critical data, keeps teams one step ahead of the decisions they need to make to optimize performance (Finario, 2026). The alternative is what most large enterprises are still living with: fragmented data, disconnected spreadsheets, and a budget conversation that’s always a few weeks out of date.

Flexibility and Accountability Aren't Opposites

One of the most persistent myths in capital planning is that you have to choose between flexibility and accountability. If you build a process agile enough to respond to market changes, you lose the governance rigor that keeps spending under control. Or conversely, that if you build rigorous controls, you lose the speed and adaptability that competitive environments demand.

This is a false dilemma. And it’s a false dilemma that’s costing organizations real money.

True accountability in capital planning doesn’t come from locking down the budget. It comes from having complete visibility into every project, what was proposed, what was approved, what was spent, and what was actually delivered against the original business case. Whether for governance or to provide a detailed history for leadership, having a comprehensive audit trail on projects large and small is not a “nice to have,” it’s foundational (Finario, 2026).

True flexibility doesn’t come from leaving the budget vague. It comes from having a process that can rapidly re-evaluate, re-rank, and re-allocate capital when conditions change without starting from scratch, and without the six-week approval cycle that turns every opportunity into a missed opportunity.

The organizations that have cracked this and exist across manufacturing, energy, food and beverage, chemicals, and beyond have one thing in common: they stopped treating capital planning as an annual finance exercise and started treating it as a continuous strategic function.

A Final Word for the Executives in the Room

If you’re a CFO, COO, or VP of Capital Projects reading this, here’s the honest version of the conversation:

The methodology debate, top-down versus bottom-up, is real. Both approaches have genuine merit and genuine failure modes. But the companies that are pulling ahead on capital efficiency aren’t winning because they picked the right side of that debate. They’re winning because they built a process sophisticated enough to transcend it.

As McKinsey has put it directly, businesses can no longer define and prepare for the future using traditional forecasting and planning methods alone. The imperative is scenario-based, dynamic capital allocation, treating investment decisions not as a once-a-year administrative exercise but as an ongoing strategic capability (McKinsey, 2025).

The good news is that the data framework, tools, and organizational playbook for doing this well already exist. The question is whether you’re willing to challenge a process that may have worked well enough in the past because “well enough” is no longer a defensible standard.

You can’t stand still while everything else is moving. Your capital planning process shouldn’t either.

Finario helps capital-intensive organizations plan, manage, and optimize their Capex investments from initial ideation through project closeout. To learn how leading enterprises are solving the flexibility-vs-accountability challenge in capital planning, learn more here.

Watch our product

overview video